INTEGRATED REPORT 2015

-

“ “A positive for the year is that we have maintained our Level 2 BBBEE status. We continue to identify, train and grow black talent...”

More from Chairman Mike Wylie -

“We have focused our attention on our procurement processes over the last 18 months and made a substantial effort to improve the quality of our order book.”

More from CEO, Louwtjie Nel

“Our Roads and earthworks and Civil engineering divisions have adapted well to the prevailing market conditions."

More from the CFO, Charles Henwood“Amid poor economic conditions, I am pleased to report that our

MIKE WYLIE, CHAIRMAN

revenue has grown to R29,5 billion and that all divisions, with one exception,

have performed well."

OUR HIGHLIGHTS

REVENUE

UP 15% to

2014: R25,7 billion

R29,5 billionCASH

UP 51% to

2014: R2,7 billion

R3,9 billionOPERATING MARGIN

DOWN to

2014: 4.0%

2.7%ROCE

DOWN to

2014: 22.7%

18.0%HEPS Continuing operations

DOWN 13.5% to

2014: 1278 cents

1106 centsLTIFR

DOWN to

2014: 0.94

0,78

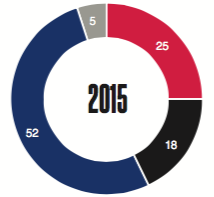

CONTRIBUTION BY SEGMENT

Revenue %

Operating profit %

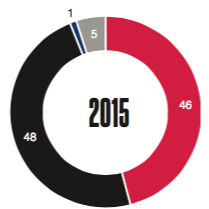

CONTRIBUTION BY GEOGRAPHY

Revenue %

Operating profit %

Building and civil engineering (including Property developments)

Building and civil engineering (including Property developments)

Roads and earthworks

Roads and earthworks

Australia

Australia

Construction materials

Construction materials

South Africa

Rest of Africa

Australia

OPERATING CONTEXT

The construction industry depends on both the public and private sectors when sourcing its projects. Being large-scale in nature, these projects entail significant capital expenditure on the part of the project owners, the funding of which is largely dependent on the economic activity within their respective environments.

GEOGRAPHIESWe operate in three distinct geographies: South Africa, the rest of Africa and Australia, servicing a broad range of building and civil engineering markets.

SOUTH AFRICA AND THE REST OF AFRICA

SOUTH AFRICA AND THE REST OF AFRICAThe emerging market, commodity-based economies of Africa, including South Africa, are particularly exposed to changes in commodity price cycles and tend to experience higher levels of market and currency volatility.

AUSTRALIA

AUSTRALIAThe Australian economy continues to demonstrate stability having delivered a 25th consecutive year of growth. Due to the high standard of living and world-class education system, Australia experiences high levels of immigration particularly from China and Asia.

MARKETS AND SECTORS

We provide our skills and services across all three geographies through our various operating divisions: Building and civil engineering; Roads and earthworks; Australia; Projects; and Construction materials.

BUILDING AND CIVIL ENGINEERING

BUILDING AND CIVIL ENGINEERING

WBHO sources the large majority of its building projects from the private sector, but is to a limited extent, exposed to the public sector through public healthcare and public, private partnerships.

ROADS AND EARTHWORKS

ROADS AND EARTHWORKS

The effects of the weakened conditions within the mining sector have also impacted the Roads and earthworks division, particularly in the rest of Africa where the majority of projects are sourced from this sector.

AUSTRALIA

Strong Asian investment continued to support activity in the residential sectors of the Australian building markets, particularly in Melbourne and Sydney.

CONSTRUCTION MATERIALS

CONSTRUCTION MATERIALS

The group’s construction materials businesses predominantly serve the local building industry and experienced improved levels of activity aligned with the stronger conditions within building markets.

PROJECTS

PROJECTS

Activity in the public, private partnership space was quiet, however due to the ongoing energy crisis a number of opportunities in the renewable energy sector are currently being explored.

MATERIAL ISSUES

The culmination of the material matter determination process is the following list of our most material issues in no particular order.

MARKET DYNAMICS

Each of the various sectors and geographies from which the group sources its projects has its own inherent risk profile and corresponding margins, as well as being exposed to differing effects from both global and regional economic cycles at different times.

SKILLS SHORTAGES AND CAPACITY CONSTRAINTS

The construction industry is faced with a serious skills shortage at various levels and so developing and retaining skilled personnel is critical to our ability to deliver projects and grow as a company.

LABOUR UNREST

The construction industry employs a sizable labour force and the labour environment is often highly politicised and volatile, particularly in South Africa where disruptions are common place.

SAFETY AND ENVIRONMENTAL MANAGEMENT

Construction is an inherently dangerous, high-impact activity. We have a duty to maintain the very highest health and safety standards to ensure employee and subcontractor welfare, morale and productivity, as well as legal compliance.

REPUTATION AND CULTURE

A positive reputation is critical to developing and maintaining the close relationships with clients that ensure repeat work and the credibility to tender on large projects successfully.

TRANSFORMATION

Transformation is a key challenge in South Africa. The construction industry benefits from significant public spending and, as a result, transformation within the sector remains high on the political agenda of the government.

COMPLIANCE

The construction industry is highly regulated. Regulatory and legal compliance is top of the governance agenda for the group. Compliance with the relevant legislation and regulations in each of the countries and sectors within which we operate is essential.

STRATEGIC OBJECTIVES

Our six strategic objectives are linked to our underlying strategic initiatives, including explicit metrics and indicators where these are available.

Our VISION is to be the leading construction company wherever we operate, being “a pleasure to do business with” by delivering quality solutions every time. We are adaptable and flexible enough to “go where the work is”, even when conditions are challenging, without compromising our standards. We navigate competitive market conditions by being flexible, dependable and hard-working and focus on nurturing strong client relationships by delivering on projects consistently.

FLEXIBILITY AND DIVERSIFICATION

Given that the construction environment is characterised by continually changing market conditions, we believe that flexibility and diversification are key attributes for success.

PROCUREMENT AND EXECUTION EXCELLENCE

Procurement and execution are simultaneous, continuous and interlinked processes within the group.

REPUTATION AND RELATIONSHIPS

A visible profile in the marketplace and our reputation for reliability, consistency and value-for-money are critical to developing and maintaining close relationships with clients and being able to tender on large projects successfully.

CAPACITY AND TALENT MANAGEMENT

A key element of construction is people management: as demand fluctuates with economic cycles so to do our resourcing requirements, meaning we are in a constant process of right-sizing our teams either upwards or downwards.

SAFETY AND ENVIRONMENTAL MANAGEMENT

Construction is an inherently dangerous, high-impact activity. As an international contractor with operations across Africa and Australia, it is imperative that we maintain the very highest health and safety standards.

LOCALISATION AND TRANSFORMATION

These objectives have become key issues on government agendas across all the geographies in which we operate.

OUR PERFORMANCE

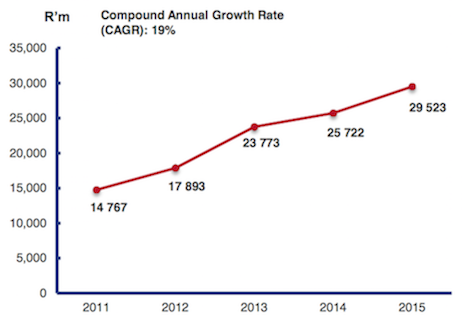

Revenue from continuing operations increased by 15% from R25,7 billion to R29,5 billion for the year ended 30 June 2015. Growth of 23% from Australia and 21% from the rest of Africa underpinned this performance, however moderate growth of 3% was also achieved by our local South African businesses.

The 23% decrease in operating profit before non-trading items from R1 billion to R793 million is primarily due to the margin of 0,1% (2014: 2%) achieved in Australia for the year, resulting in a decrease in the overall margin from 4% to 2,7%.